Key Provisions in the One Big Beautiful Bill Act

July 2025

On July 4, 2025, President Donald J. Trump signed the One Big Beautiful Bill Act into law. This document provides a summary of key provisions of the legislation and outlines potential impacts for stakeholders.

Tax Cuts & Extensions

- Permanent Extension of Individual Tax Provisions under the 2017 TCJA: The bill makes the individual income tax rate cuts and related benefits from Tax Cuts and Jobs Act permanent.

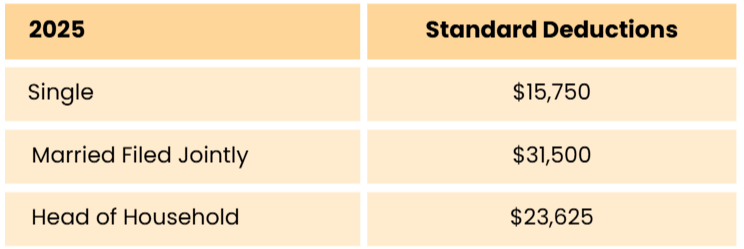

- Increase in standard deduction by $750 ($1,500 for couples):

- Permanent AMT Exemption Increases with Phaseout Reversion: This measure permanently extends the higher AMT exemption levels while reverting phaseout thresholds to 2018 levels.

Bonus Senior Deductions (Age 65 and Older)

- Taxpayers 65 and older can claim an extra standard deduction of $2,000 for singles and $1,600 per qualifying spouse on top of the standard deduction (no income limit).

- Taxpayers 65 and older earning up to $75,000 (singles) and $150,000 (couples) qualify for an additional standard deduction:

- $6,000 additional deduction for singles

- $12,000 additional deduction for couples

- This is a temporary benefit between 2025 and 2028.

Federal Estate Tax Exemption

- Estate Tax Exemption Increase: Beginning in 2026, the estate tax exemption will rise to $15 million per individual and $30 million per couple.

- The exemption will be adjusted annually for inflation.

SALT Deduction Cap

- The state and local tax (SALT) deduction cap has been raised to $40,000 (from $10,000) for married couples earning up to $500,000 through 2029.

- The $40,000 cap decreases by 30% of any modified adjusted gross income (MAGI) exceeding $500,000. This continues until the cap reaches $10,000 for incomes at or above $600,000.

Auto-loan Interest Deduction

- From 2025 to 2028, up to $10,000 in annual interest on new auto loans will be tax-deductible.

- The vehicle must be US-assembled.

- Phases out at $100,000 for individuals and $200,000 for couples.

Child Tax Credits

- Child Tax Credit raised to $2,200 per child (from $2,000).

- Income thresholds: $200,000 for singles, $400,000 for joint filers.

- A one-time $1,000 credit will be provided for each child born between 2025 and 2028, deposited into a new tax-advantaged savings account.

529 Plan Benefits

- Expanded K-12 Withdrawal Limit: Annual 529 withdrawal limit for K-12 expenses increased to $20,000.

- Broader K-12 Eligible Uses: 529 funds now cover tutoring, textbooks, online learning, and homeschool materials.

- Expanded Postsecondary Coverage: Eligible uses now include credentialing and registered apprenticeship programs.

- Permanent ABLE Plans: Section 529A Achieving a Better Life Experience Act (ABLE) accounts have been made a permanent part of the tax code.

Charity Deductions

- Charitable Deduction for Non-Itemizers: Allows a deduction of $1,000 ($2,000 for couples) for charitable contributions without itemizing.

- Income-Based Requirement: Deduction eligibility requires a minimum contribution based on income level.

- AGI Deduction Limits: The charitable deduction limit for cash remains at 60% of AGI. The deduction limit stays at 30% of AGI for most gifts of appreciated assets.

- New AGI Floor: Beginning January 21, 2026, itemizers will face a new 0.5% AGI floor on charitable deductions. This means only the portion of total charitable contributions that exceeds 0.5% of adjusted gross income (AGI) will be deductible.

Itemized Deduction

- Top Tax Bracket Deduction Cap: The tax benefit of itemized deductions for taxpayers in the top bracket (37%) is capped at $0.35 for each dollar.

Tip Income & Overtime Pay

- Tip Income Deduction: Allows a deduction of up to $25,000 annually for reported tips from 2025–2028; phases out above $150,000 ($300,000 for joint filers).

- Overtime Pay Deduction: New deduction of up to $12,500 for single filers ($25,000 for joint filers) on overtime pay, effective 2025–2028; phases out above $150,000 ($300,000 for joint filers).

Student Loans

- Graduate Loan Limits: Annual loan limit of $20,500 with a lifetime maximum of $100,000 for graduate students.

- Professional Program Loan Caps: Capped at $50,000 per year and $200,000 total for professional programs (e.g., medical, law).

- Parent PLUS Loan Limits: Annual maximum of $20,000 and a lifetime cap of $65,000 for Parent PLUS loans.

- Effective Date: Loan limits apply to borrowers beginning July 2026.

Qualified Business Exemption Income

- Permanent Pass-Through Deduction: The 20% deduction for pass-through businesses is now permanent.

- Minimum QBI Deduction: Taxpayers with at least $1,000 in active qualified business income (QBI) are guaranteed a minimum $400 deduction.

- Increased Phase-In Thresholds: Phase-in thresholds raised to $75,000 for singles and $150,000 for couples.

Radiation Exposure Compensation Act (RECA)

- The recently expired RECA has been reauthorized through December 31, 2028.

- Eligibility has been expanded for victims of radioactive waste exposure, and compensation amounts have increased.

- Individuals impacted in counties in Utah, New Mexico, Arizona, Idaho, and communities in Missouri, Tennessee, Alaska, and Kentucky are now covered.

- Individuals residing in affected areas for at least two years with specified diseases may qualify for compensation.

- Individuals impacted in counties in Utah, New Mexico, Arizona, Idaho, and communities in Missouri, Tennessee, Alaska, and Kentucky are now covered.

- Eligibility for uranium workers is extended through 1990.

- Eligible individuals now qualify after one year of residence or employment in impacted zones.

Natural Disaster Relief

- The bill permanently revives and extends the TCJA-era treatment of disaster-related personal casualty losses for federally or state declared disaster zones.

- Natural catastrophes include any hurricane, tornado, storm, high water, wind-driven water, tidal wave, tsunami, earthquake, volcanic eruption, landslide, mudslide, snowstorm, or drought, fire, flood, or explosion.

- Individuals who suffered damage in such zones can now deduct losses without the 10% of AGI floor, making relief available even to non-itemizers. Losses must exceed $500.

- The expansion is retroactive to disasters declared in the previous year, enabling people affected by earlier events to amend past returns and claim deductions.

Other Changes

- Farmland Sales: Capital gains from farmland sales can now be paid via installment method without acceleration upon sale.

- The farmland must be sold to a farmer who will continue to farm the land for ten years after the sale.

Capital gains payments can be spread over four years.

- The farmland must be sold to a farmer who will continue to farm the land for ten years after the sale.

- Business Interest Deduction: Expanded for small businesses and real estate investors (specifics pending IRS guidance).

- Qualified Opportunity Zones: Made permanent. New reporting requirements and expansion to additional census tracts.

- Qualified Small Business Stock (QSBS) Expansion: Section 1202 now includes businesses with up to $100 million in gross assets (previously $50 million), and holding period reduced to three years for certain tech/startup sectors. This only applies to stock issues after July 4, 2025.